Managing small business cash flow is perhaps one of the major headaches that you will have as a business owner. Cash flow which refers to the influx and outflux of cash within your business is critical in meeting costs of operation, expansion and stability. Research conducted by U.S. Bank solicits that lack of internal cash flow management is one of the greatest reasons as to why some businesses fail with 82% of the failure reason attributed to cash flow problems in business affairs.

The good thing is that managing and enhancing business cash flow does not have to be a complicated task. With proper practical and common sense approaches, your finances can be handled and all your processes can be seamless. The article presents an overview of useful techniques aimed at the optimization of cash flow management among small business owners to enhance their chances of success in business for a long period of time.

Understand Your Cash Flow

Cash flow in business can be defined as the flow of funds in and out of your business. It has two main components:

- Inflows – Money that comes into your business as customer payments, loans, or investments.

- Outflows – Money going out in the form of payments in respect of rent, salaries, supplies, utilities cost and others.

Positive cash flow simply means you have more gross reception than you have expenditure and it’s a good balance for every business.

How Often Cash Flow Should be Monitored?

Monitoring the cash flow of your small business provides you with a good picture of your cash and how it is used. Continual monitoring allows you to:

- Prevent tragic situations where cash runs dry.

- Take advantage of cash surplus where there’s an opportunity to save or invest.

- Determine if there is a need to increase or scale back in business activities.

Failure to keep track of this can lead to late payments, failure to leverage opportunities or even insolvency.

To assist in this, use applications and systems that cater to cash flow management for small businesses. Programs like QuickBooks, Xero, or Wave enable you to receive information regarding your income and expenditure without strain. Such systems offer cash flow planning and monitoring through timely reports, which improves effectiveness in managing cash flows in business.

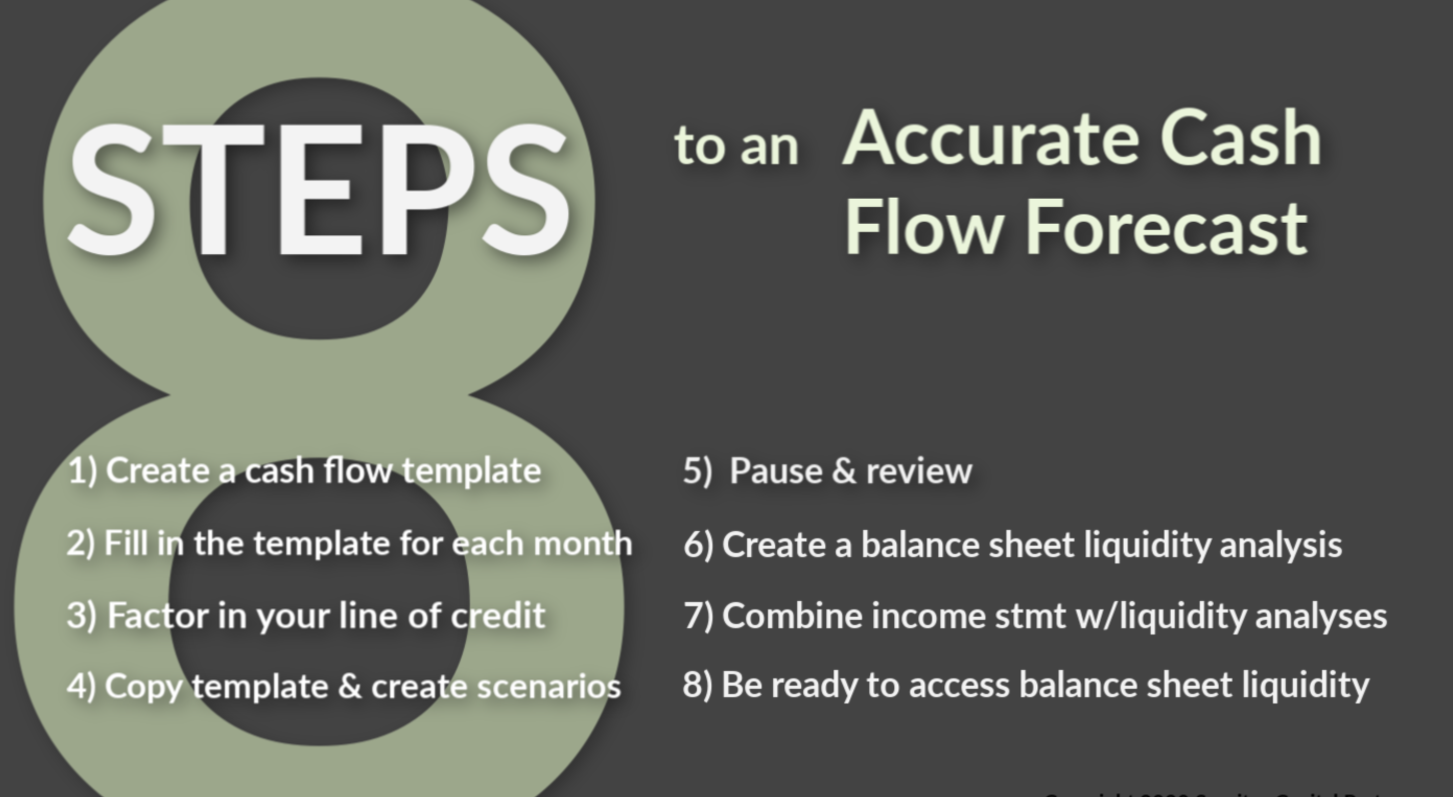

Create a Cash Flow Forecast

Managing small business cash flow effectively can be challenging, but a cash flow forecast can make a big difference. A cash flow forecast is a financial tool that predicts your future cash inflows (like sales or client payments) and outflows (like expenses or loan repayments). By forecasting, you can plan ahead, avoid cash shortages, and make smarter financial decisions for your business.

Steps to Build an Accurate Cash Flow Forecast

- Track Your Inflows: Start by listing all expected income, such as sales revenue, investments, or loans.

- List Your Outflows: Include fixed expenses like rent, utilities, payroll, and variable costs like supplies or marketing.

- Choose a time frame: Monthly forecasts are common for small businesses, but you can go weekly for more precision.

- Use Reliable Tools: Use spreadsheets or cash flow software to organize data for accuracy and clarity.

Analyze and Adjust: Compare your forecast against the actual cash flow in your business to spot patterns and refine your predictions.

Why You Should Update Your Forecast Regularly

A cash flow forecast isn’t a one-time task. Regular updates are essential because cash flow in business can change quickly. Unexpected expenses or delayed payments can throw off your forecast, but revisiting it frequently lets you adjust for new trends and maintain control. Aim to update your forecast monthly or whenever major changes occur in your business.

Optimize Payment Processes

Managing your small business cash flow effectively starts with optimizing how you get paid. Delayed payments can create bottlenecks in your business cash flow, but a few simple changes can make a big difference. According to a QuickBooks report, 61% of small businesses consistently face cash flow challenges, and only 52% of invoices are paid on time, highlighting the importance of proactive management of receivables and payables.

1. Start with Early Invoicing and Clear Payment Terms

Invoices should be issued within the shortest time possible after the job is done or the product is sold. The bills will be paid faster when they are issued faster. Always explain to your customers the payment terms and be clear on the contract due date on every invoice, late fees and acceptable payment methods. This is because transparency fosters trust amongst the clients and lowers the chances of misunderstandings which in turn assists ease the cash flow in business.

2. Follow Up on Overdue Payments

Overdue payments should be pursued without any regrets. When clients become late in payment, a gentle reminder email or phone call may be all it takes to get them to do something. Alternatively, use payment solutions that have automated notices. For clients that are consistent late payers, suggest that they be given discounts for early payments or be penalized for late payments. Invoking such measures helps to ensure that cash flow in the business is adequately safeguarded.

3. Offer Multiple Payment Options

Make it simple for your clientele to make payments by providing them with several options. Apart from the usual option of bank wire, credit cards, e-wallets or other payments applications should be made available. The more options available, the quicker the payments will come in and your small business will maintain a positive cash flow.

By fine-tuning your payment processes, you’ll ensure steady cash flow in business operations and reduce financial stress. Start implementing these tips today to see the impact on your business cash flow.

Manage Expenses Effectively

Managing your expenses effectively is crucial to improving your small business cash flow. Every dollar saved is a dollar that can be reinvested into growing your business. Here are some actionable steps to help you cut costs and maintain better cash flow in business.

Start by reviewing your monthly expenses. Are there subscriptions, services, or tools you’re paying for but rarely use? Cancel or downgrade them to save money. Even small cuts can add up significantly over time. For example, opting for a shared workspace instead of a private office can reduce overhead costs without compromising productivity.

Your suppliers want your business, and many are willing to negotiate. Approach them with a clear understanding of your purchasing needs. Request bulk discounts, extended payment terms, or promotional offers. Even small savings here can significantly improve your small business cash flow.

Make it a habit to regularly review your operational expenses. Look for inefficiencies—are you overpaying for utilities or insurance? Switching providers or renegotiating contracts could lead to significant savings. By staying proactive, you can keep your small business cash flow under control and allocate funds to more critical areas.

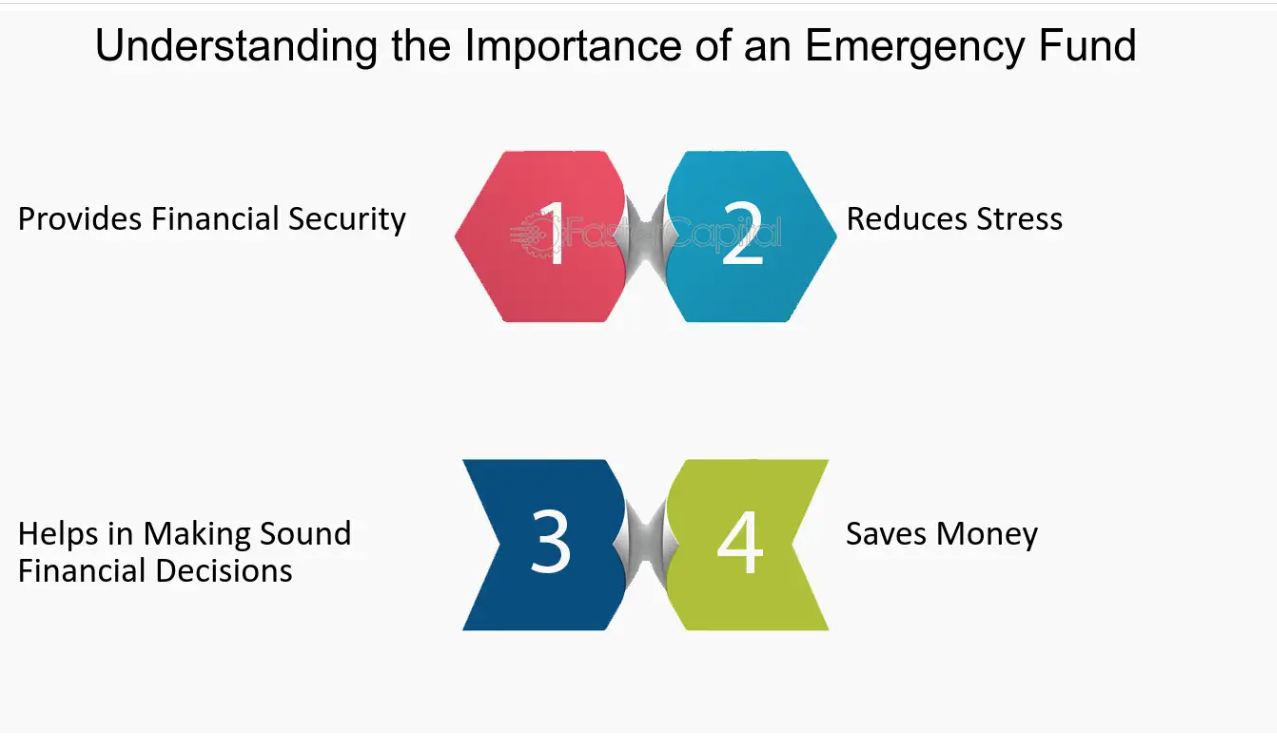

Build a Cash Reserve

As a small business owner, managing small business cash flow can be tricky. One of the best ways to safeguard your business is by building an emergency fund, or a cash reserve. Having a cash reserve ensures you’re prepared for unexpected events, like sudden drops in revenue or unplanned expenses. It provides a cushion that keeps your business cash flow steady during tough times and helps you avoid relying on loans or credit.

Why Is an Emergency Fund Important?

A solid emergency fund is crucial for maintaining healthy cash flow in business. According to research, nearly 60% of small businesses face challenges with managing cash flow. By setting aside a portion of your earnings regularly, you create a safety net that can be a lifesaver when cash flow dips unexpectedly.

How to Build Your Cash Reserve Gradually

- Start Small and Be Consistent: You don’t need to set aside large amounts right away. Begin with 1-2% of your monthly revenue, and gradually increase it as your business grows. The key is consistency.

- Set a Goal: Aim to save 3-6 months of operating expenses. This amount varies based on your business type, but having this goal helps you stay motivated and focused.

- Automate Savings: Automate transfers to a separate savings account. This ensures you’re always setting money aside without thinking twice.

- Reinvest in Your Reserve: As you experience positive small business cash flow, put a percentage back into your cash reserve until you reach your target.

Leverage Financing Options Wisely

As a small business owner, maintaining a healthy cash flow is essential to keeping your operations running smoothly. However, there may be times when you face cash flow gaps, and that’s when short-term financing can be a helpful tool.

Short-term financing options like business lines of credit, merchant cash advances, and short-term loans can provide quick access to funds. These options can help you cover expenses like payroll or inventory, allowing you to keep the business moving forward during slow periods.

However, don’t over-rely on loans or credit. While they can solve immediate cash flow issues, they also come with interest and fees, which can strain your finances in the long run. Relying too heavily on borrowed money can lead to a cycle of debt that’s difficult to break, impacting your small business cash flow.

Before committing to any financing option, it’s crucial to understand the terms. Pay attention to interest rates, repayment schedules, and any hidden fees. Knowing these details ensures you don’t end up with a deal that hurts your business cash flow more than it helps.

Monitor and Adjust Regularly

Managing cash flow in business is a continuous process, not a one-time task. As a small business owner, you need to monitor your cash flow regularly to ensure that your business stays financially healthy. Cash flow is the lifeblood of your operations, and understanding its ebb and flow can help you avoid unexpected shortfalls.

Start by analyzing cash flow trends over time. Are your inflows consistent? Are there periods when cash is tight? Identifying patterns will allow you to predict future cash needs and make adjustments before issues arise. For example, if you notice a dip in cash flow during certain months, you can plan for it by adjusting payment schedules or cutting non-essential costs.

But monitoring on your own can only get you so far. Consulting a financial expert can offer invaluable insights. They can help you refine your cash flow forecasting, identify potential financial risks, and suggest strategic adjustments that you might have missed. Experts can also guide you in leveraging financial tools to manage small business cash flow more effectively.

Position Cash Flow Management as a Long-Term Strategy

Improving cash flow in business is essential for the success and growth of any small business. By understanding your small business cash flow, forecasting accurately, optimizing payments, managing expenses, and building a reserve, you can ensure financial stability. Regularly monitoring and adjusting your business cash flow is equally important to stay ahead of challenges. With these steps in place, you’ll not only improve your small business cash flow but also set your business up for long-term success. Stay proactive, informed, and committed to maintaining healthy cash flow management practices.

Featured Image by FreePik